Following our previous discussion, as AI enters its fourth year of accelerated development—driving equity markets to new highs and prompting enterprises to ramp up capital expenditures—investors are beginning to focus on two more fundamental questions:

- Can AI sustain its 2025 level of high-growth momentum into 2026?

- Are the AI investments companies have "committed" to already showing signs of declining capital efficiency and extended payback periods, suggesting the early stages of a valuation bubble?

For people who haven’t read our previous article: 2026 Outlook Series Part 1 – What’s Next for the Global Economy in the Age of AI

We believe AI will remain the central theme of 2026, but the industry has clearly entered a new phase—shifting from broad-based narrative-driven gains to a more competitive period of outcome verification and structural divergence. In other words, investor focus is transitioning from “Are you in AI?” to “Can you deliver irreplaceable, structural value in compute expansion and real-world deployment?” Capital will increasingly flow toward segments with limited supply, high technical barriers, pricing power, and profit scalability.

Based on this, Part 2 of our “2026 Outlook Series” will explore how continued AI hardware investment is shaping Taiwan’s semiconductor industry—unpacking the next wave of growth drivers, potential shifts in investment cycles, and identifying which parts of the supply chain are most likely to benefit structurally as capital efficiency becomes a more scrutinized metric.

Key Industry 1: ASIC

While ASIC (Application-Specific Integrated Circuit) technology has been around for years, the true industry inflection point has come from hyperscalers (CSPs) ramping up their in-house chip design efforts. As AWS, Google, Meta and others bring custom ASIC projects into volume production in 2026, the ASIC industry is poised to begin realizing significant commercial results.

ASIC Advantage: Lower Inference Costs

Custom Chips with Power and Cost Efficiency

ASICs are custom-designed chips built for specific workloads. While not a new technology, they have long been deployed in performance- and cost-sensitive sectors like automotive and networking. Their key features include high computational efficiency, low power usage, and the lowest cost per unit workload.

| Feature | GPU | ASIC |

|---|---|---|

| Purpose | General-purpose compute | Optimized for single task |

| Performance | Balanced | Maximized for specific tasks |

| Power Usage | High | Low |

| Cost | High | Low (high upfront cost) |

| Flexibility | High | Low |

| Key Use Cases | Gaming/AI training | Mining/AI inference/networking |

To reduce reliance on NVIDIA, CSPs are accelerating the development of in-house ASICs.

In the early stages of the AI boom, ASICs were not the primary compute solution for cloud service providers (CSPs). Due to their powerful general-purpose capabilities, GPUs remained the preferred choice for large-scale model training. However, as generative AI rapidly scaled between 2023 and 2024, NVIDIA quickly dominated the compute market through strong performance and a mature software-hardware ecosystem, creating a highly concentrated supply landscape.

To mitigate dependency risks—and with AI workloads shifting from training toward high-volume inference—CSPs began investing more aggressively in custom ASIC development. With clear advantages in power efficiency, cost, and performance optimization, ASICs have become a key strategic path for CSPs seeking to diversify their compute infrastructure.

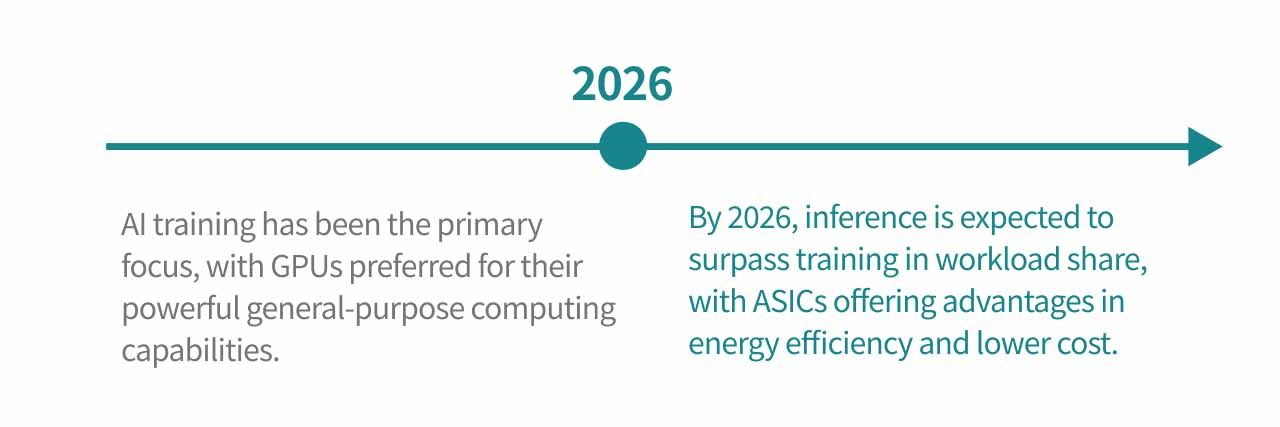

AI Shifts from Training to Inference – ASIC Gains Momentum

Before 2025: Training Dominated AI Investment

In the early stages of AI development, the industry was almost entirely focused on "building the model first." Cloud providers and model developers largely pursued the scaling law—expanding data and parameter size—as the primary path forward, treating training capabilities as a key competitive moat. As a result, capital expenditures and compute resources were heavily concentrated in repeated pretraining and iterative retraining of a few large foundation models.

Within this context, GPUs—with their mature software ecosystem and general-purpose computing flexibility—dominated the AI accelerator market up to 2023. Industry revenue was also skewed toward the training side. In contrast, custom ASICs designed for specific workloads and commercial services centered on large-scale inference remained in early-stage testing and had not yet become part of the mainstream investment narrative.

As models such as GPT-4, Gemini, and Claude began to stabilize, AI entered a "model maturation phase" in 2024–2025. Training and inference began developing in parallel: on one hand, models and data continued to scale and new versions were trained; on the other, inference APIs and cloud service demand surged.

However, even with inference traffic growing visibly, AI accelerators prior to 2025 were still largely focused on training in terms of both CapEx and compute cycles, keeping GPUs as the CSPs’ preferred choice. But as inference began to take up a larger share of the workload, the structural advantages of ASICs—lower total cost of ownership (TCO), higher energy efficiency, and reduced latency—started to stand out, accelerating the momentum behind ASIC adoption.

2026: Inference Becomes the Core Compute Demand

As large-scale models such as ChatGPT and Gemini continue to iterate and mature in terms of performance and functionality, the industry's focus has shifted from “building the model” to “how to deliver it to more users and use cases at lower cost and higher efficiency.”

According to research by Fubon, AI workloads are now clearly divided into training and inference. Looking ahead, compute demand will shift from CapEx-heavy, large-scale training tasks toward inference-driven workloads, which run continuously across enterprises and end-user devices. Beginning in 2026, inference is expected to surpass training in workload share, with the gap widening over time. While training remains essential, it has become more of a periodic, large-scale CapEx event. In contrast, inference is now the primary source of compute demand, powered by 24/7 operations across tens of thousands of businesses and hundreds of millions of end users.

With inference becoming the dominant compute battleground, CSPs are adopting AI ASICs at scale to reduce total cost of ownership (TCO), energy consumption, and latency. Industry estimates suggest ASICs offer approximately 30% lower cost than GPUs, and starting in 2026, ASICs are projected to outpace GPUs in both growth rate and unit shipments, driven by an explosion in inference volume.

In specific workloads, ASICs provide significantly better power efficiency and performance. While GPUs offer flexibility, they are less energy-efficient and come with a higher TCO. In practical comparisons, the TCO gap between GPU and ASIC for the same inference task can reach up to 2.44x. For instance, AWS reports its Trainium ASIC is around 30% cheaper than equivalent GPUs, and Google’s TPU v7 server costs are nearly 30% lower than the GB300 platform, further highlighting ASICs’ structural advantages in performance per dollar and power usage.

As inference volume continues to surpass training beyond 2026 and operating expenses (OPEX) rise, a hybrid architecture—using GPUs for training and ASICs for large-scale inference—will become essential to optimize AI infrastructure in terms of TCO and energy efficiency.

TCO, Total Cost of Ownership TCO represents the full cost of owning an asset across its entire lifecycle—from initial acquisition to end-of-life. This includes not only upfront build costs, but also the ongoing training, maintenance, upgrades, and eventual retirement or replacement costs.

Related Articles: NVIDIA Acquires Groq's Inference Technology License for $20 Billion

2026 ASIC Industry Outlook

2025: Tape-Out Heavy, Limited Volume Production—2026 to See Major Ramp-Up

ASIC development cycles are relatively long. Inference-focused AI ASICs typically require 10–12 months from design to first tape-out, while larger training ASICs can take 15–24 months. With added complexity from custom SoC design, HBM integration, and 2.5D/3D advanced packaging, actual timelines are often extended further.

As a result, although 2025 saw a surge in ASIC design, verification, and tape-out activities, relatively few projects entered full-scale production, and revenue contributions remained limited. 2025 served as a “setup year” for next-generation 3nm/2nm ASIC projects focused on design and tape-out, while most production still centered around 5nm/4nm chips with HBM3.

Looking ahead to 2026–2027, newer ASICs will transition to 3nm nodes paired with HBM3e/HBM4, significantly boosting compute per chip and memory bandwidth. This will mark the beginning of mass production and shipment for XPU-related designs built on those nodes.

For example:

- AWS shipped ~1.25 million AI ASIC units in 2025; with Trainium 3 ramping up in 2026, shipments are expected to reach ~1.51 million (+20.8% YoY).

- Google shipped ~1.75 million TPU units in 2025; following the TPU v7 ramp in 2026, shipments could reach ~3 million (+71.4% YoY).

2026: New Customer Adoption Reshapes Growth Structure

2025: Growth Driven Primarily by CSP In-House Projects

ASICs are designed for specific applications and deliver clear advantages in efficiency and power consumption, but they also come with high upfront development costs, long design cycles, and risk of design failure. Early on, only large CSPs with sufficient technical and financial resources could afford to invest in custom chip development. As a result, 2025 growth was largely driven by existing CSP projects, with a highly concentrated customer base.

2026: New Entrants Fuel TAM Expansion

As AI adoption deepens across industries, many companies are developing custom ASICs tailored to their own workloads to reduce deployment costs and build differentiated capabilities. In addition to major CSPs, Bytedance, OpenAI, and Apple have launched in-house chip initiatives, often in collaboration with ASIC design service providers.

This influx of new customers is significantly expanding the Total Addressable Market (TAM) for AI ASICs.

According to Fubon’s estimates:

- In 2024, the cloud AI ASIC market was valued at $10–12 billion

- By 2026, the market is expected to grow to $30–35 billion

- This equates to 2.5–3.5x growth over two years, or a ~70% CAGR

Three Core Growth Drivers for 2026’s High-Growth Cycle

- Shift from Training to Large-Scale Inference As inference becomes the dominant workload in AI deployment, demand for optimized inference ASICs will surge.

- Volume Ramp of 3nm/2nm CSP Projects Leading-edge projects from AWS, Google, and other hyperscalers begin entering mass production with enhanced performance and memory capabilities.

- Entry of New Customers like Bytedance, OpenAI, and Tesla These players are accelerating custom chip development, expanding demand beyond the initial CSP-driven base.

Together, these drivers are expected to push total ASIC unit shipments up by ~37% YoY in 2026. Higher demand for performance and power efficiency is also lifting ASP (Average Selling Price), adding to revenue momentum.

In summary, the AI ASIC industry is transitioning into a high-volume, high-demand growth phase, with a projected 70% CAGR from 2024 to 2026, marking a structural inflection point for the sector.

Taiwan: Key Beneficiaries in the ASIC Supply Chain

The ASIC supply chain can be divided into three major stages: front-end design, back-end design, and manufacturing & packaging/testing. In Taiwan, most players are concentrated in back-end design and foundry services, where per-unit margins are relatively lower, meaning profitability depends heavily on large-scale volume shipments to drive revenue.

While new customers are expected to enter the ASIC market starting in 2026, the primary growth engine will still come from volume ramp-ups in large CSP projects. As such, Taiwan’s ASIC sector in 2026 should focus on companies that have secured CSP projects and are moving successfully into mass production, as they stand to benefit the most from this wave of structural expansion.

Alchip Technologies (3661.TW)

Alchip is one of Taiwan’s leading ASIC design service providers, specializing in back-end design with the highest global market share in the segment. Its business model revolves around NRE (Non-Recurring Engineering) + MP (Mass Production), with a revenue mix heavily skewed toward high-performance computing (HPC) applications.

Competitive Advantages:

- Long-standing collaboration with TSMC

- Proven track record with major CSPs

- Cost-competitive pricing enabled by a focus on back-end services

2026 Growth Drivers:

- AWS 3nm ASIC project enters full production, significantly boosting revenue

- Li Auto’s 5nm automotive chip ramps up to mass production

- Strong contribution from networking and cryptocurrency-related projects

Despite some delays in the 3nm ramp (now expected in 2Q26), Alchip is well-positioned for a breakout year in 2026, making it a key beneficiary of structural AI ASIC growth.

Global Unichip Corp. (3443.TW)

GUC, a TSMC-affiliated company, focuses on advanced ASIC design services and provides end-to-end solutions, including Spec-in, SoC integration, physical implementation, 2.5D/3D packaging, and HBM / chip-to-chip interconnect IP. Its core business model is NRE + Turnkey, with Turnkey accounting for over 60% of revenue, complemented by high-margin IP licensing and technical services.

Competitive Advantages:

- Strong process synergy and capacity support from TSMC

- Deep integration capabilities on advanced packaging platforms

- Broad exposure to leading CSPs and AI customers

2026 Growth Drivers:

- Google CPU, Microsoft, and Meta AI accelerator projects transition into Turnkey mass production from 2H26

- HBM3E enters volume production, with co-development of HBM4 IP alongside memory vendors, contributing high-margin IP and design service revenue

- Sustained demand in cryptocurrency applications provides notable revenue support

In summary, GUC combines deep ties to TSMC, strength in advanced packaging and IP, and diversified exposure to AI and CSP clients, making it a core structural beneficiary of the ongoing AI ASIC expansion trend.

Up next, we’ll break down another key sector: thermal management (cooling solutions) — don’t miss it!

2026 Outlook Series Part 3 – Key Industry: Thermal Management